Time to Revamp Livestock Pricing?

At a livestock industry conference last week, the main topic covered was outlook—both for feed and livestock/meat. However, the most lively discussions revolved around price reporting. Everyone knows formula pricing now is dominant over “negotiated” cash prices, but producers may not appreciate the extent to which this is the case.

Consider this: The percent of hogs sold in the spot market was 62% in 1994. By 2000, it had fallen to 26%. In 2013 and again in 2014, the percentage was 3. Even more significantly, the formula price is based on the spot market. So virtually every hog delivered is priced off 3% that are “negotiated.”

In some regions, concentration in ownership adds to the lack of transparency regarding cash prices. Day after day in recent months, USDA’s National Daily Hog and Pork Summary has reported no carcass base price for the morning Eastern Corn Belt hog run because numbers are low enough that it would endanger the confidentiality of the seller. Usually—but not always—the numbers creep high enough by the end of the day for an average price to be reported. On April 20, for instance, 2,620 receipts were issued on a carcass basis but no price was reported.

The same April 20 report showed just 56 receipts in Iowa/Minnesota reporting live price, against 1,286 carcass price.

The spreads between futures, carcass and live prices also sometimes inject uncertainty as market participants await some convergence between futures and cash. The April 20 closing price on the nearby May futures contract was $70.28, the national carcass base price was $61.18, while the live price was $47.40. After a weak trading day, Alan Brugler of Brugler Marketing and Management commented, “May futures are waiting for cash to catch up.”

Looking at the cattle market, Brugler noted that the annual trading range for live cattle futures has averaged $19.46 since 1996. However, last year, the range was more than $37—almost double. Implied volatility, which surged in early 2015, now is dropping to more normal levels.

In recent months the spread between feedlot asking prices and packer bids has been wide every week. As a result, few or no cash bids take place before Thursday; in some cases Friday. This leaves the market wondering where the value lies.

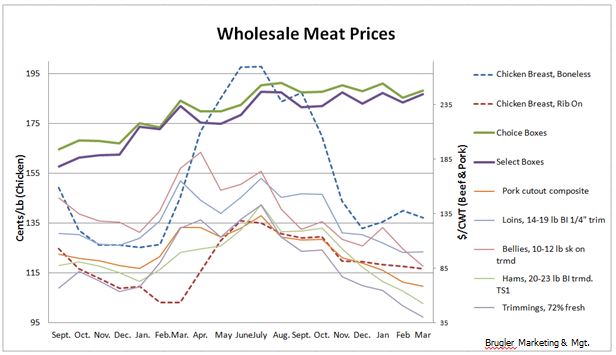

There also are a lot of unknowns regarding shifts in beef grades, attendees at the meeting noted. More than three-quarters of beef now grades Choice or better. “The top third of the Choice is cherry picked by branded programs,” one attendee said, noting that because of the higher percentage grading better, hamburger supplies are comparatively tight. That has caused the Choice-Select spread to narrow to a very slim difference at time this year. “It doesn’t pay to feed to Choice at a $3 spread,” one feeder commented.

Perhaps more important in the big scheme of things is the tremendous and growing spread in prices among the meats, however. “At what point will the consumer throw some pork or poultry on the grill instead of beef?” is the question that has traders on edge.